Post office savings schemes have quietly built wealth for millions of Indians over decades. Among the most searched comparisons right now is PLI or RD which is better — and it makes sense why people are asking. Both carry government backing, both offer reliable returns, and both are accessible through post offices across the country.

But they serve fundamentally different purposes. Understanding those differences is what actually helps you choose. In this article, we have discussed the difference, benefits, eligibility and more details about both of them to help you choose better.

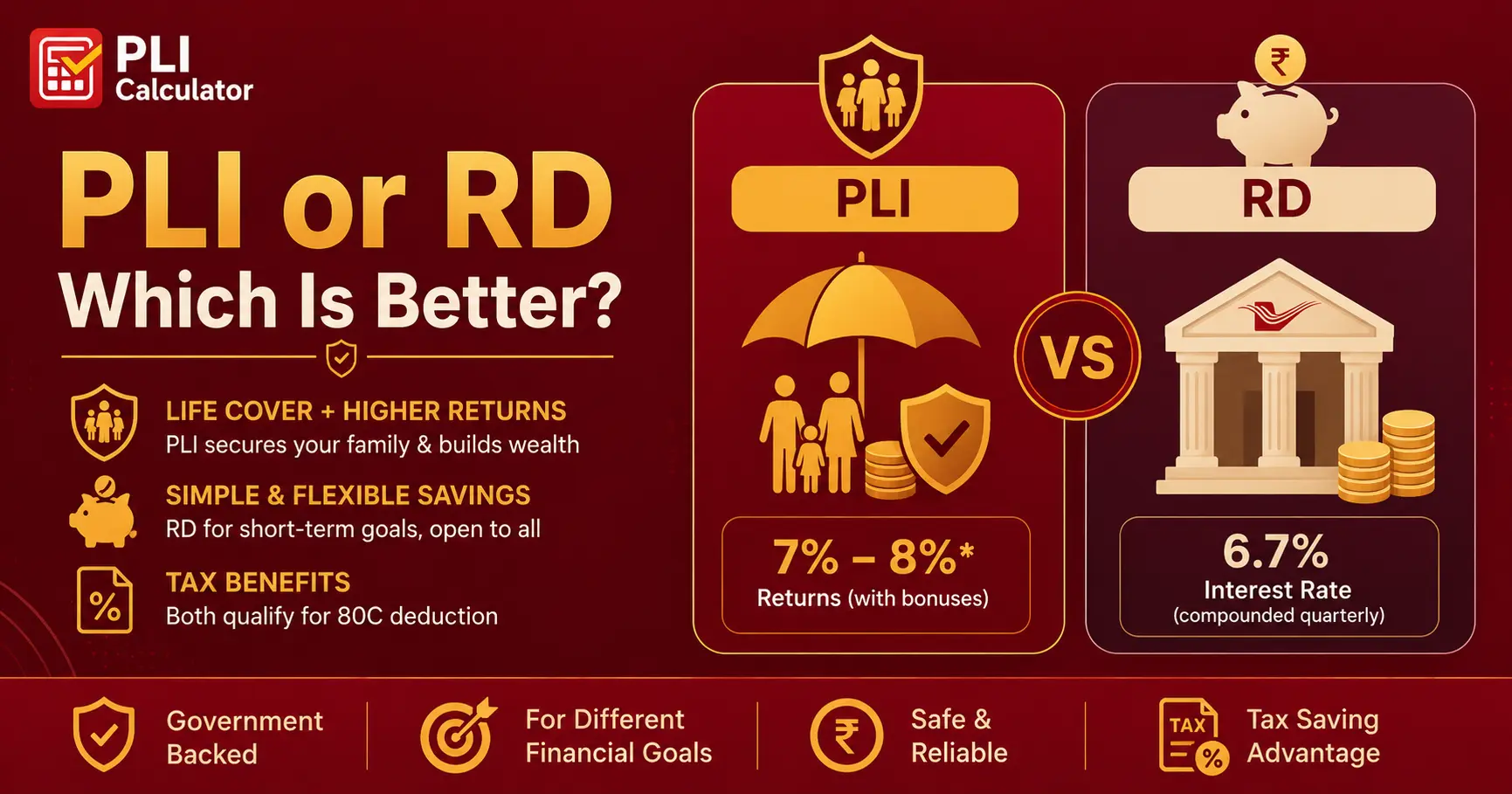

What Is PLI?

Postal Life Insurance (PLI) is one of India’s oldest insurance-linked savings schemes, available exclusively to government and select public sector employees. It isn’t just a savings tool — it combines life coverage with long-term wealth accumulation.

The longer your policy runs, the more the bonus compounds. That’s a meaningful advantage for anyone with a 15–20 year financial horizon.

Who Can Apply for PLI?

- Central and state government employees

- Defence and paramilitary personnel

- Employees of nationalised banks and financial institutions

- Teachers at government-aided schools and universities

If you don’t fall into these categories, PLI simply isn’t an option for you — which immediately narrows the PLI vs RD debate for a large section of the population.

What Is Post Office RD?

A Post Office Recurring Deposit is a monthly savings scheme open to any Indian resident. You commit a fixed amount every month — starting as low as ₹100 — for a tenure of five years. At the end, you receive your principal back with interest.

The post office RD interest rate currently stands at 6.7% per annum, compounded quarterly. It’s not spectacular, but it’s stable, government-guaranteed, and predictable — which matters a lot for conservative savers.

There is no life cover involved. What you put in grows at a fixed rate, and that’s the deal. Simple, transparent, and accessible to everyone.

📖 Read More Related Blog

⚖️ PLI vs PPF: Returns, Tax Benefits & Maturity Comparison 2026Complete comparison — returns, tax savings & maturity value →

PLI vs RD: A Direct Comparison

These two products don’t compete on equal ground because they’re built for different needs. Still, comparing them side by side clarifies things quickly.

Understanding the PLI Maturity Calculator

Before committing to a PLI policy, it helps to estimate what you’ll actually receive. The PLI maturity calculator is an online tool — available on India Post’s official website — that computes your maturity amount based on:

- The type of PLI plan chosen (Endowment, Whole Life, etc.)

- Sum assured

- Policy tenure

- Your age at entry

Using the Post office PLI maturity calculator before signing up gives you a realistic picture of your returns. Many people skip this step and later feel uncertain about whether they made the right choice. Running the numbers takes five minutes and removes that doubt entirely.

📖 Read More Related Blog

⚖️ PLI vs SIP: Complete Comparison of Returns, Risk, and Tax BenefitsLooking for the best investment option? This PLI vs SIP comparison explains returns, safety, tax benefits, and wealth growth →

Which One Should You Actually Choose?

There’s no universal answer, but the decision becomes straightforward once you’re honest about your situation.

You want life cover bundled with long-term savings

You have a 15–20 year horizon and can stay committed

Maximising tax-free maturity benefits matters to you

You want simple, flexible monthly savings without insurance

You prefer a shorter, fixed five-year commitment

You’re building an emergency corpus or saving for a specific goal

For many salaried government employees, carrying both actually makes sense. PLI handles the insurance and long-term wealth angle, while RD takes care of short-to-medium term savings goals running in parallel.

A Practical Way to Think About It

Imagine a government school teacher saving for their child’s education five years away. An RD makes perfect sense — fixed monthly deposits, known maturity date, guaranteed returns. Now imagine the same teacher also wanting life cover for their family’s security over the next 20 years. That’s where PLI steps in.

The two aren’t always in competition. Sometimes they’re complementary.

📖 Read More Related Blog

📋 RPLI vs PLI: Eligibility, Benefits & Key Differences ExplainedWho can apply & how RPLI differs from PLI →