PLI (Postal Life Insurance) and SIP (Systematic Investment Plan) are two fundamentally different financial tools serving distinct wealth-building purposes. PLI combines insurance protection with investment returns, while SIP is a disciplined investment approach focused on market-linked growth.

Understanding PLI vs SIP is crucial because choosing the wrong one can significantly impact your returns, protection, and tax efficiency over time. In this article, we will discuss PLI vs SIP which is better, compares actual returns using real numbers, explains risk profiles, and helps you understand tax implications. Read this article till end for the complete details with comparison of returns and tax benefits about both of them.

What is PLI and What is SIP?

Understanding PLI (Postal Life Insurance)

PLI is a government-backed life insurance plan combining insurance coverage with investment returns:

- Life insurance protection for your family

- Annual bonus payouts accumulating over your policy term

- Government backing ensuring complete fund safety

- Tax benefits under Section 80C on premiums

- Fixed maturity amount including sum assured plus accumulated bonuses

PLI typically runs 10–25 years with bonus rates of ₹40–₹76 per ₹1,000 sum assured, delivering 5.5%–7% effective annual returns.

📖 Read More Related Blog

⚖️ PLI vs PPF: Returns, Tax Benefits & Maturity Comparison 2026Complete comparison — returns, tax savings & maturity value →

Understanding SIP (Systematic Investment Plan)

SIP is an investment methodology involving fixed regular contributions into mutual funds:

- Disciplined investing with fixed monthly contributions

- Market-linked returns fluctuating with market performance

- Rupee cost averaging reducing market volatility impact

- High flexibility to adjust or stop contributions anytime

- Higher return potential compared to traditional fixed-income instruments

Side-by-Side Comparison

| Parameter | PLI | SIP |

|---|---|---|

| Type | Insurance + Investment | Pure Investment |

| Return Rate | Fixed (5.5%–7%) | Market-dependent (5%–15%+) |

| Risk Level | Very Low | Low to High |

| Life Insurance | Included | Not included |

| Lock-in Period | 15–25 years | None |

| Liquidity | Limited | High |

| Tax Benefits | Section 80C | Section 80C + LTCG |

| Government Backing | Yes | Depends on fund |

| Minimum Investment | ₹100–₹500/month | ₹500–₹1,000/month |

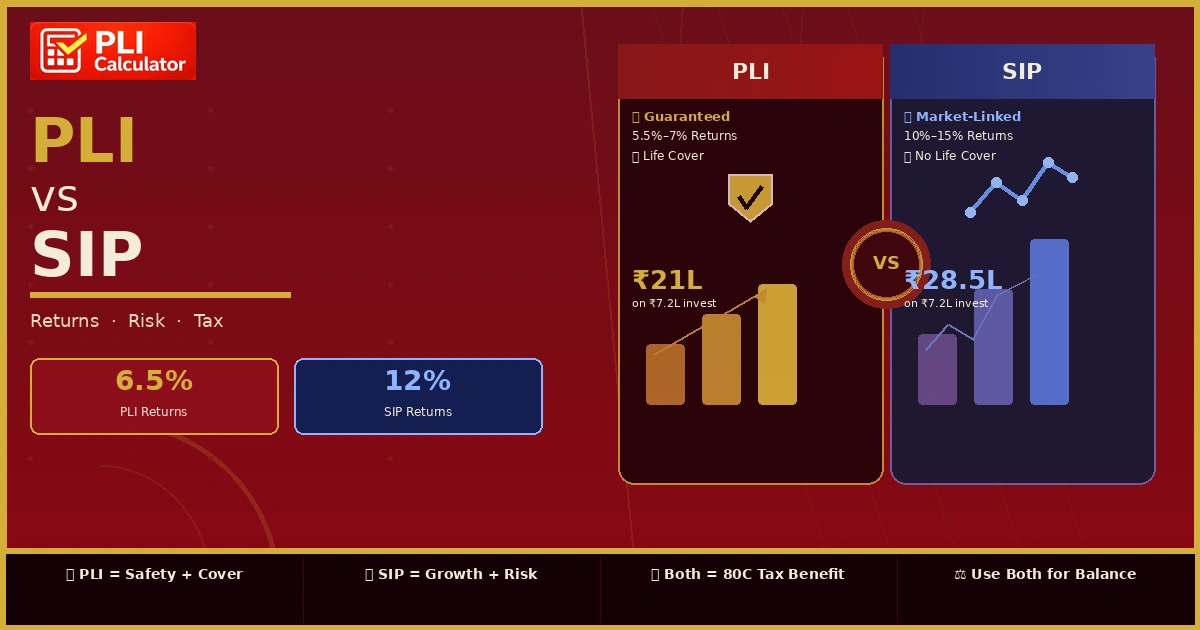

Real Returns Comparison

PLI Returns Example

- Monthly premium ₹3,000

- Sum assured ₹10,00,000

- Policy term 20 years

- Bonus rate ₹55 per ₹1,000

Sum assured: ₹10,00,000

Annual bonus: ₹55,000

Total bonus (20 years): ₹11,00,000

Final maturity: ₹21,00,000

Effective return: ~6.5% annually

📖 Read More Related Blog

📋 PLI Interest Rate 2026: Updates, Features & EligibilityCheck interest rates, maturity benefits & how PLI works →

SIP Returns Example

- Monthly SIP ₹3,000

- Period 20 years

- Average annual return 12%

Final maturity: ₹28,50,000 (approximate)

Effective return: 12% annually

Total gain: ₹21,30,000

Tax Benefits Comparison

Advantages of PLI

- Section 80C deduction on premiums

- Completely tax-free maturity amount

- Tax-free bonus payouts

- Simple tax filing

Advantages of SIP

- Section 80C deduction (ELSS funds only)

- Long-term capital gains taxed at 20% with indexation

- Special dividend tax treatment

- More tax-saving mechanisms

In simple terms, PLI offers simpler tax benefits, while SIP requires more tax planning.

Risk Comparison

Risk Profile of PLI

PLI is extremely safe because:

- Government-backed by India Post

- Fixed bonus structure minimizes uncertainty

- Guaranteed sum assured at maturity

- No market risk exposure

- Predictable returns regardless of economic conditions

Risk Profile of SIP

SIP risks depend on fund selection:

- Equity SIP: Market volatility, non-guaranteed returns, economic sensitivity

- Debt SIP: Interest rate risk, credit risk, inflation erosion

📖 Read More Related Blog

📋 How to Choose the Best PLI Plan in 2026: Benefits, Bonus & Eligibility ExplainedLooking for the Best PLI Plan in 2026? Explore benefits, bonus details, eligibility criteria →

Using Calculators

PLI vs SIP Calculator

Compare final maturity amounts side-by-side based on your monthly investment and duration.

Post Office PLI Calculator

Project exact PLI maturity, annual bonus accumulation, and surrender values.

PLI Maturity Calculator

Understand bonus impact, compare plan variants, and plan retirement income precisely.

Conclusion

PLI vs SIP which is better depends on your goals, not universal superiority. PLI excels when needing guaranteed returns and life insurance. SIP shines for higher growth potential. Many successful investors maintain both. By using tools like the PLI vs SIP Calculator and Post Office PLI calculator, you’ll gain clarity to make an informed decision tailored to your financial goals.