Postal Life Insurance (PLI) is a government-backed life insurance scheme offered by India Post that combines insurance protection with investment returns. If you’re trying to understand how this scheme actually functions and what makes it different from other insurance options, this guide will walk you through every detail. PLI has been serving millions of Indian families for decades, providing affordable life coverage bundled with savings benefits that grow over time.

The PLI scheme operates on a straightforward principle which means, you pay regular premiums, and in return, you get life insurance protection plus annual bonuses that accumulate throughout your policy term. In this article, you will understand that how PLI scheme works which is important to know before you invest.

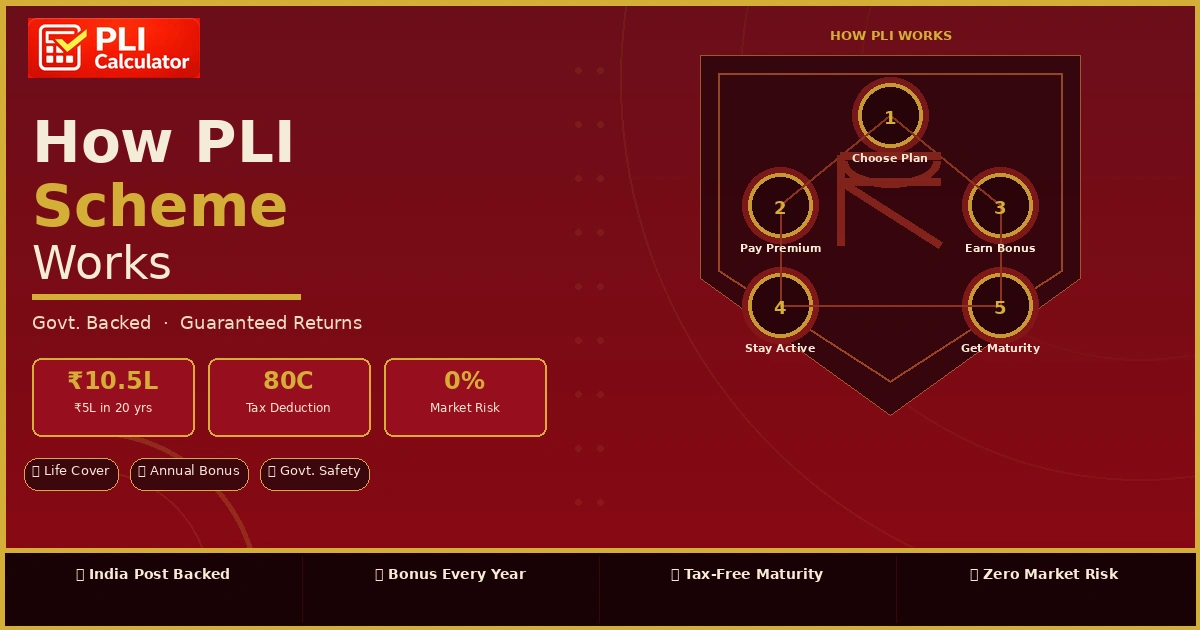

How PLI Scheme Works?

The PLI scheme functions differently from traditional insurance or pure investment products:

📖 Read More Related Blog

📋 How to Calculate PLI Maturity Amount Manually — Formula ExplainedDiscover How to Calculate PLI Maturity Amount using formula, bonus, and examples →

PLI Scheme Benefits

Life Insurance Protection

Guaranteed Returns

Tax-Free Maturity

Affordable Premiums

Government Backing

Flexibility & Loans

No Medical Tests

PLI Scheme Features

| Feature | Details |

|---|---|

| Offered By | India Post (Government of India) |

| Policy Term | 10 to 25 years depending on plan |

| Age Eligibility | 19 to 55 years (60 for Whole Life) |

| Sum Assured | ₹1,000 to ₹5,00,000+ |

| Premium Payment | Monthly, quarterly, or annual |

| Bonus Declaration | Annually per ₹1,000 sum assured |

| Maturity Payout | Sum Assured + Accumulated Bonuses |

| Tax Status | Completely tax-free |

| Loan Option | Available after 3-4 years |

| Surrender Value | Eligible after 3 years |

Understanding Different PLI Schemes

PLI Santosh Scheme (Endowment Assurance)

The PLI Santosh scheme is the most popular variant, offering balanced insurance and savings with a fixed maturity period (10, 15, or 20 years). You receive the sum assured plus bonuses as a lump sum at maturity, and your nominees get immediate benefits if you pass away during the term. It is best for people seeking guaranteed returns with life insurance and a definite maturity date.

PLI Suraksha Scheme (Whole Life Assurance)

The PLI Suraksha scheme provides lifelong protection till age 85 or 90. Unlike Santosh, this plan continues as long as you pay premiums, with bonuses accumulating throughout your lifetime. It is best for people seeking permanent life insurance coverage for their family’s long-term security.

PLI Sumangal Scheme (Anticipated Endowment)

The PLI Sumangal scheme returns your money 5 years before the actual policy term ends. If you opt for 20 years, you receive maturity after 15 years while maintaining full coverage. It is best for people wanting earlier access to accumulated funds without waiting for the full term.

PLI Yugal Suraksha Scheme (Joint Life Assurance)

The PLI Yugal Suraksha scheme covers two lives (typically married couples) under one policy with a single premium. The survivor receives the sum assured when the first life ends. It is best for married couples seeking joint protection with shared premium responsibility.

PLI Suvidha Scheme (Convertible Whole Life)

The PLI Suvidha scheme starts as term assurance and converts to whole life coverage after the initial term. This provides flexibility as your needs change over time. It is best for people uncertain about long-term needs wanting upgrade options.

PLI Bal Jeevan Bima Scheme (Children’s Policy)

The PLI Bal Jeevan Bima scheme covers children from birth to age 25. Parents pay premiums, and at age 25, children receive sum assured plus accumulated bonuses. It is best for parents to build a financial corpus for children’s education and future needs.

📖 Read More Related Blog

📋 How to Choose the Best PLI Plan in 2026: Benefits, Bonus & Eligibility ExplainedLooking for the Best PLI Plan in 2026? Explore benefits, bonus details, eligibility criteria →

How PLI Works in Real?

- Sum assured ₹5,00,000

- Policy term 20 years

- Monthly premium ₹2,000

- Annual bonus rate ₹55 per ₹1,000

- Total investment ₹4,80,000 (₹2,000 × 12 × 20)

- Annual bonus ₹27,500 (₹5,00,000 × 55/1,000)

- Total bonus over 20 years ₹5,50,000

- Maturity amount ₹10,50,000 (₹5,00,000 + ₹5,50,000)

- Profit ₹5,70,000

The PLI scheme works as a comprehensive solution combining affordable life insurance with guaranteed investment returns. Whether you choose PLI Santosh scheme for fixed maturity or PLI Suraksha scheme for lifelong coverage, understanding how the scheme operates helps you make informed decisions. Start early, pay consistently, and let compound bonuses build your wealth while protecting your family’s financial future.

Frequently Asked Questions (FAQs)

How does a bonus work in PLI scheme?

India Post declares annual bonus rates per ₹1,000 sum assured; this accumulates every year and is paid as a lump sum at maturity.

What happens if I miss a premium payment?

Your policy lapses, but you can revive it within 12 months by paying outstanding premiums plus revival charges.

Can I withdraw money before maturity?

Yes, after 3-4 years you can take loans against your policy or surrender it for 30-50% of premiums plus bonuses.

Is PLI better than bank fixed deposits?

PLI offers similar returns (5.5%-7%) to FDs but includes life insurance protection; FDs provide only savings.

What are PLI’s tax benefits?

Premiums are deductible under Section 80C up to ₹1.5 lakh annually, but entire maturity is completely tax-free.